Bond Valuation.Talking about fixed income is not talking about complex concepts and terms that cannot be explained in two or three sentences. Price calculation is not complex. However, if we want to analyze every detail that affects the price, a more in-depth study is required on concepts such as duration , modified duration and sensitivity (explained in detail later).

A premise before starting, we have to understand that fixed income is not fixed, or rather, the rate of return that we obtain from investing in a bond will only be the one initially calculated if we keep it until maturity. In other words, the price of the bond is subject to the volatility of interest rates (remember that the price of a bond moves inversely to the movement of interest rates) and therefore the effective return will not have to coincide with the one fixed at the time of purchase.

At this point, we must distinguish between:

- Fixed coupon bonds: This type of securities periodically distributes a fixed coupon. For example, 5% per year. They are normally distributed semi-annually. So if a bond with a nominal 1,000 euros has a fixed coupon of 5% it will distribute 25 euros every six months.

- Zero coupon bond : This type of security does not pay interest until the maturity date, that is, it delivers the interest together with the loan amount at the end. In compensation, its price is lower than its nominal value, that is, it is issued at a discount, which gives a greater return to the principal.

- Floating coupon bond : These are securities that provide their interest at a floating rate, linked to the evolution of a money market interest rate (euribor, libor …) plus a differential. Example: Euribor + 2%.

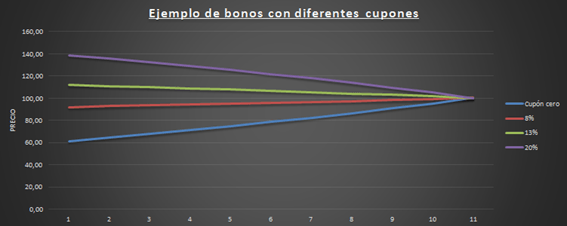

Graphically we represent a zero coupon bond and three bonds with fixed coupons (20%, 13% and 8%), with maturity of 100. That is why, depending on the price at which a bond is issued and its coupon, it may be above par ( above 100) or under torque (below 100).

Formulas to calculate the price of a bond and examples

The valuation of a fixed income bond requires a methodical process and some knowledge of the financial laws of capitalization and discount .

Coupon bond valuation

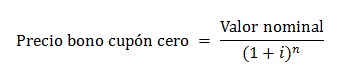

The present value of a bond is equal to the cash flows that will be received in the future, discounted at the present time at an interest rate (i), that is, the value of the coupons and the nominal value as of today. In other words, we have to calculate the net present value (NPV) of the bond:

Or what is the same:

Example of calculating the price of a coupon bond

For example, if we are on January 1 of the year 20 and we have a two-year bond that distributes a coupon of 5% per year paid semi-annually, its nominal value is 1,000 euros that will be paid on December 31 of the year 22 and its rate of discount or interest rate is 5.80% per year (which means 2.90% biannual) the intrinsic value of the bond will be:

If the interest rate is equal to the coupon, the price of the bond exactly matches the nominal value:

If we know the price of the bond but we do not know what the interest rate is, we have to calculate the internal rate of return (IRR) of the bond .

Solving for “r” we obtain that: r = 2.90% (which would be 5.80% per year)

Couponless Bond Valuation

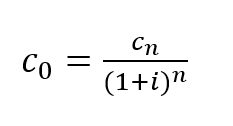

The valuation of the zero coupon bonds is the same but easier, since there is only one future cash flow, which we will have to discount to know the current value:

Example of calculating the price of a zero coupon bond

For example, if we are on January 1 of the year 20 and we have a zero coupon bond that has a nominal value of 1,000 euros, an exact maturity of 2 years (it will pay 1,000 euros on December 31, 2022) and an interest rate of 5 Annual% the price will be:

The calculation of the price of floating coupon bonds is more complex since we do not know the coupons to be paid and therefore we will have to make estimates.

On the other hand, for the examples above we have used exact dates. When several days have passed the calculation is the same, but we have to calculate the days remaining and the coupon run .

If the bonds have call options ( callable bond ) we will have to subtract the option premium from the price and if they have put options ( putable bond ) we will have to add the option premium.

Example calculation of a bond price with excel

However, thanks to the tool (download excel at the end of the document) we will try to facilitate the calculations.

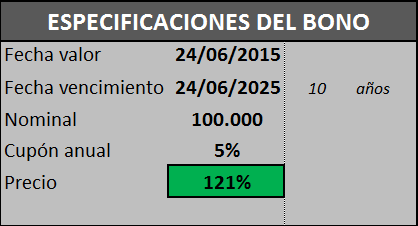

First, we have the bonus data:

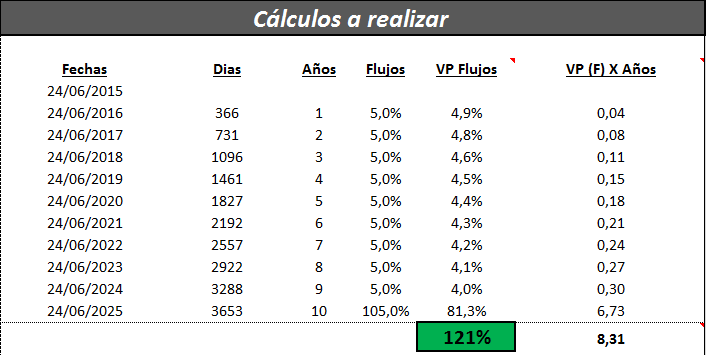

We can verify that it is a bond that is issued today (the Excel will update to date automatically) and with a duration of 10 years. With a nominal value of 100,000 monetary units, an annual coupon of 5% and its purchase price is 121% above the nominal.

Second, we want to calculate the duration of the bond in question. For this we have used the valuation by calculating the cash flows and giving a value to each one according to the time duration.

By columns (see table below), we have:

- Dates: which is equal to today’s date or value date that we have in the bond specifications. Consecutively we have annually, the coupon payment dates (annual) until the maturity of the bond.

- Days: this is the number of days that are far from today’s date or value date to that cash flow in question.

- Years: it will be necessary to convert the days into years, dividing them by 365, which is the number of days that a year has (the valuation is made “current – current” by market convention).

- Flows: these are the expected cash flows, remember that we will receive 5% of the annual coupon and when due we will receive the 5% coupon + 100% of the nominal amount.

- Present value of flows: at this point, we use the compound discount law. We want to know by discounting each flow that we have previously calculated at the interest rate.

- Cn: cash flow (in our case 5% and maturity 105%).

- i: the current interest rate given for that price of the bond.

- n: the years that we have previously calculated.

- Present value of cash flows for the corresponding time period (years): that is, we calculate the duration in years of each cash flow and then add them together and obtain the duration of the bond in its entirety.

In the following table we show you the calculations made:

Finally, we come to the analysis and evaluation part:

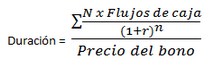

Duration can be defined as the weighted average of the different moments in which a bond makes its payments, using as a weight the current value of each of the flows divided by the price of the bond. This weighted average will be expressed in the same unit in which we measure maturities, the most common being expressed in years.

The Modified Duration consists of evaluating how the value of a fixed income security changes due to the change in market interest rates. Contrary to duration, which is measured in years, the modified duration is measured in percentage terms, and indicates the percentage of change in the value of a fixed income asset when market interest rates change by one percentage point.

Sensitivity is the first derivative of the expression that relates the price of a bond with its IRR. In a fixed income asset with fixed coupons, the absolute sensitivity includes the absolute change that occurs in the price of the asset in the face of unit absolute changes in the IRR of the asset, that is, it reflects the profit or loss, in monetary units, in the face of changes absolute returns. Absolute sensitivity can be compared to one of the meanings of the delta in financial options , in which it defines the delta as the variation of the premium in the face of infinitesimal movements in the underlying asset.

Absolute sensitivity is used as a measure of risk in the management of fixed income assets. Unlike duration, whose measurement is in years and, therefore, its sign is always positive (you cannot go to the past), the absolute sensitivity is given in monetary units.