The recovery period discounted or discounted payback is a dynamic method of evaluating investments that determines when the money from an investment is recovered, taking into account the effects of the passage of time on money.

It is a liquidity criterion, which is equivalent to the simple recovery period or payback , but discounting the cash flows. It is about subtracting discounted cash flows from the initial investment until the investment is recovered and that year will be the discounted payback.

Represents the time it takes to recover the investment, taking into account the moment in which the cash flows occur. It also has some problems such as not taking into account the cash flows that occur from each period after having recovered the investment.

Therefore, it is configured as an adequate method to evaluate risky investments that allows completing the analysis carried out with profitability criteria ( NPV or IRR ).

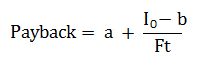

Discount Payback Formula

The easiest way to calculate it is through a spreadsheet. But we can also calculate it with the simple payback formula once we have discounted the periods at the current time. This is the formula to calculate it:

Where:

- a: It is the number of the immediately previous period until the initial disbursement is recovered

- I 0: It is the initial investment of the project

- b: It is the sum of the flows until the end of period «a»

- Ft: It is the value of the cash flow of the year in which the investment is recovered

Discounted payback example

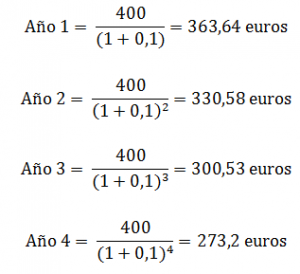

Let’s suppose that we made an investment of 1,000 euros in year 1 and, in the next four years, at the end of each year we receive 400 euros. The discount rate that we will use to calculate the value of the flows will be 10%. Our undiscounted cash flow scheme will be:

-1000 / 400/400/400/400

To calculate the value of each of the periods we will take into account the year in which we received them:

In year 1 we received 400 euros, which discounted one year after the investment (year zero) are worth 363.63 euros. Discounting all the cash flows, we obtain the following discounted flow scheme:

-1000 / 363.64 / 330.58 / 300.53 / 273.2

If we add the flows for the first three years we obtain 994.75 euros. Remaining 5.25 euros remain to be recovered. Now we apply the simple payback formula:

Discounted payback = 3 years + 5.25 / 273.2 = 3.02 years

Under this investment scheme, it will take 3.02 years to recover the disbursed money.

According to the simple payback they would be: 1000/400 = 2.5 years

If we compare the discounted payback, we see that the simple payback will tell us that we are recovering the investment before (2.5 years), while the reality is that it will take 3.02 years using 10% as a discount rate. This is because money has less value in the future, as long as the discount rate is positive.