The convexity of a bond is the slope of the curve that relates price and profitability. It measures the change in the duration of the bond as a result of a change in profitability.

Mathematically it is expressed as the second derivative of the price-return curve. The formula is as follows:

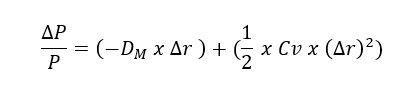

The variation in the price of a bond due to changes in interest rates is the sum of the variation motivated by the modified duration and the variation motivated by the convexity of the bond.

If the convexity of a bond is equal to 100, the price of the bond will vary by 1% extra every 1% of variation in interest rates, in addition to that calculated for the duration. If the convexity of a bond is equal to zero, the price of the bond will vary due to changes in interest rates the amount motivated by the duration of the bond.

Convexity of a bond and duration of a bond

The convexity of a bond offers us a much more accurate measure of the price-return changes of a bond. The duration of a bond assumes that the relationship between price and profitability is constant. However, the reality is very different. Hence, given small variations in price-performance, the duration is an acceptable measure. But for larger variations the calculation of convexity is essential.

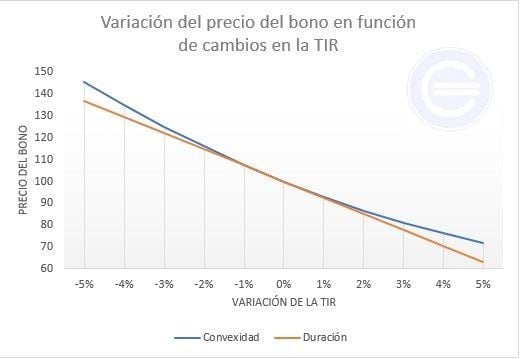

Mathematically it may seem like a slightly abstract term. Since graphically it is much easier to understand, let’s see it represented. In the following two graphs we see both duration and convexity represented.

The lower the return on the bond, the higher its price. And vice versa, the higher the return on the lower bond will be its price. Of course, the price does not change in the same proportion if its profitability changes from 10 to 12% than if it changes from 1 to 2%. This is what convexity takes into account. The duration assumes that the change in price is the same always. While convexity takes into account that the change in price is not constant. The difference between the blue and the orange line is the convexity itself. The orange line is the change in the price of the bond taking into account the duration. Finally, the blue line represents the changes in the price of the bond taking into account duration and convexity.

Convexity example of a bond

We have a 10-year bond. The coupon is 7% and the bond has a nominal value of 100 euros. The IRR of the market is 5%. Which means that bonds with similar characteristics are offering a 5% return. Or what is the same 2% less. Coupon payment is annual.

If the yield on the bond goes from 7% to 5%, how much does the price of the bond vary? To calculate the variation that the price would have before a change in the interest rate we will need the following formulas:

Bonus price calculation :

Calculation of the duration of the bonus :

Modified duration calculation:

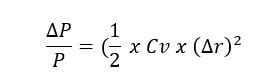

Convexity calculation:

Calculation of the variation of the duration:

Calculation of the convex variation:

Calculation of the variation of the bond price:

Download Excel table to see all detailed calculations

Using the formulas mentioned above we obtain the following data:

Bonus price = 115.44

Duration = 7.71

Modified Duration = 7.34

Convexity = 69.73

The variation of the price in the face of a 2% drop in the yield of the bond is + 14.68% taking into account the duration. The variation in the price of the bond taking into account convexity is + 1.39%. To obtain the total price variation we must add the two variations. The calculation shows that given a 2% drop in this bond, the price would increase by 16.07%.