The unit labor cost (CLU) is a measure that indicates what it costs to employ a worker based on the productivity of the company. That is, it is the fraction of the productivity that the employer has to divert to the remuneration of the salaried work that he hires. They are the salary costs necessary to produce each unit.

To do this, it relates the remuneration per employee (RAU) with productivity (PT). The formula defines the unit labor cost such that:

So the unit labor cost is composed of the ratio between two variables. The first, the salary per employee, which is calculated as the sum of all wages (RA) in a territory between the number of employees (As). The result it shows would be something like the average salary.

The second part of the equation, productivity , is calculated as the ratio between gross domestic product (GDP) and the employed population (PO).

Interpretation of the Unit Labor Cost

An increase in the unit labor cost is interpreted as an increase in labor costs. And, therefore, an obstacle to ensure the return of the invested capital. On the contrary, a reduction in Unitary Labor Cost reflects a reduction in the labor force. Which is a facility to ensure the return of the invested capital.

The Unit Labor Cost may be reduced due to the following situations:

- If the average salary (RAU) falls and productivity (PT) remains constant, the CLU is reduced.

- If the average salary (RAU) remains constant and productivity (PT) increases, the CLU is reduced.

- If the average salary (RAU) falls and productivity (PT) increases, the CLU is reduced.

- If the average salary (RAU) falls in greater proportion than productivity (PT), the CLU is reduced.

- If the average salary (RAU) increases to a lesser extent than productivity (PT), the CLU is reduced.

The Unit Labor Cost may increase if:

- The average salary (RAU) increases and productivity (PT) remains constant. CLU increases

- The average salary (RAU) remains constant and productivity (PT) falls. CLU increases

- The average salary (RAU) increases and productivity (PT) falls. CLU increases

- The average salary (RAU) falls to a lesser extent than productivity (PT). CLU increases

- The average salary (RAU) increases in greater proportion than productivity (PT). CLU increases

Finally, the Unit Labor Cost remains constant provided that:

- The average salary (RAU) increases in the same proportion as productivity (PT). Constant CLU

- The average salary (RAU) is reduced in the same proportion as productivity (PT). Constant CLU

- The average salary (RAU) remains constant and productivity (PT) as well. Constant CLU

Example of the unit labor cost calculation

After the previous explanation we will see a practical example that helps us understand how to calculate the Unitary Labor Cost of Spain.

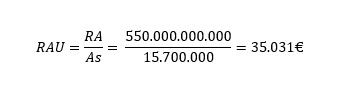

- Compensation of employees (RA): 550,000,000,000

- Number of employees (As): 15,700,000

- Employed population (PO): 18,800,000

- Gross Domestic Product (GDP): 1,232,000,000,000

First we will calculate the numerator (upper part) of the Unitary Labor Cost ratio:

Next, we will calculate the denominator (bottom) of the Unitary Labor Cost ratio:

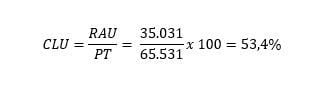

Once we have both results, we substitute in the initial formula:

The result reflects that of the total profits that an entrepreneur has in Spain, on average, he must allocate 53.4% to pay salaries.